Remember that White House shouting match—Donald Trump, two other blokes, all ganging up on a wartime President?

Well, it got me thinking: what was the mining industry making of all the rare earths buzz that may decide the fate of the western world? Or the world at large.

Enter Amanda Lacaze, CEO of Lynas—the world’s top rare earths producer outside China. I’ve admired her straight-shooting style since we met a few years ago at Fortune’s Most Powerful Women International in Hong Kong. We bonded over Australia, the Aussie sense of humour and the beautiful contradictions of Asia.

So, when her latest earnings call landed just as Ukraine’s so-called “deal of the century” hit the headlines, I tuned in.

Her take?

Rare earths in Ukraine? Much ado about nothing:

Transcript: “In all the time I’ve been in Rare earths, I’ve heard about everything from a rare earths race to the moon because there could be lots of mining on the moon because there could be lots of rare earths.

I’ve heard about a rare earths race to the sea floor because there is lots of rare earths on the sea floor that could be useful in the future. I heard about a rare earths race to Afghanistan at one stage. There is always a lot of discussion on these matters.

I remember watching a television show with my husband and they were talking about accessing Lanthanum and how expensive it was. And I’m like, well I’ve got 100 tonnes in the warehouse if you’d like to come buy some from me.

So our view on this is - and I think Everybody who assesses this industry would know how long it takes from having the thought bubble of, ‘Wouldn't it be great to have some rare earths sourced from X?’ Wherever X may be! And actually having some separated product sitting in a big bag waiting for a customer to buy it.

Our view, very simple- To get guaranteed supply in the West, is to buy product from Lynas because we have it. We have the resource at Mt Weld, and we have the skills to process that resource cost efficiently. So we don’t get too tied up with the speculation about the various different sources of rare earths. We just really focus on what we do is the best that we can.”

The Real Rare Earths Game

As my political economics professor at the Maxwell School of Citizenship & Public Affairs probably would have put it: the real action isn’t in speculation—it’s in supply, demand and pricing; but most critically - policy.

Over the past two years rare earths pricing plummeted from their 2022 high despite demand, thanks to China.

According to Amanda, China’s recently announced industry reforms could shift the market - prices are starting to inch up since.

Lynas, meanwhile, is expanding its Mount Weld mine in Australia to boost production in 2025. Lynas is one of 2 of the largest players outside China who can deliver ‘processed’ rare earth supply. That means Australia’s role in global supply is set to grow, with its share projected to hit 18% by 2030.

So, How Rare Are Rare Earths?

Not as rare as the name suggests—10 of the 17 elements are common. The problem?

- They're usually spread out thinly in rocks, not concentrated in one place.

- It's hard and expensive to separate them from other elements.

Why should we care?

Rare Earths are needed in pretty much every electronic product we use. From guided missiles to healthcare and the latest phone in our hand. The list below gives us a clear idea - just how important these elements are in keeping the engine of an economy and our own personal lives ticking!

Considering the lynchpin for all this currently is a dependence on China, many companies are starting to find alternatives:

• Apple: uses rare earth elements such as neodymium, praseodymium, and dysprosium primarily in the magnets found in its devices. Itwill use 100% recycled rare earths in all magnets by this year, 2025.

• Tesla: uses neodymium, praseodymium, and dysprosium and claims it will cut rare earth use in its EV motors and is aiming to eliminate them entirely. No details have been given by the company

• BMW: is already using some rare-earth-free electric motors.

But it is undeniable. Rare earth demand is here to stay. With the global energy transition surging, demand for lithium and cobalt for example is skyrocketing. By 2045, clean energy tech will account for:

🔋 90% of lithium demand

🔋 70% of cobalt demand

🔋 40% of rare earths demand

Who Actually Has Rare Earths

In the good old days (pre-Trump 2.0) The Minerals Security Partnership (MSP)—a U.S.-led coalition including Australia, Canada, the EU, and Ukraine—aimed to secure critical minerals supply chains.

According to the US, which is one of the MSP's founding partners, the MSP's purpose is to ensure that critical minerals “are produced, processed and recycled in a manner that supports the ability of countries to realize the full economic development benefit of their geological endowments.”

Where the U.S. under the Trump administration will finally land up within the alliance is anyone’s guess.

My bet? It will probably go the way of the Paris Agreement.

So, where are the biggest reserves everyone is trying to shore up?

🥇 China – 44M metric tons

🥈 Brazil – 21M metric tons

🥉 India – 6.9M metric tons

🇦🇺 Australia – 5.7M metric tons (Lynas territory!)

🇷🇺 Russia – 3.8M metric tons

🇺🇸 USA – Just 1.9M metric tons, but still the 2nd largest producer

🇬🇱 Greenland: 1.5M metric tons (bet you didn’t see that one coming!) Why hasn’t it been mined yet, you ask? Enormous capital outlay to get the basic infrastructure to even build a mine. According to the IEEE Spectrum's report - they’d need to build a deepwater port just to get started. And then there are the weather conditions to contend with.

Speaking to IEEE Spectrum - American Rare Earths’ board member and newly appointed Co-Chair of the Critical Minerals Institute (CMI) Melissa Sanderson explained, “Greenland is an exceptionally difficult area in which to mine. Temperatures, snow, ice, etcetera. And of course, in the spring, such as it is, there are oceans of mud.”

Production: Who’s Really in Charge?

When it comes to mining, China dominates. But the real power is in processing, and China owns 90% of that market.

🏆 China – 240K metric tons (nearly 70% of global production)

🥈 USA – 43K metric tons (but the only operational mine is partly Chinese-owned, and processing historically has been all China).

🥉 Myanmar – 31K metric tons - A major supplier to China, Myanmar is dealing with serious supply chain instability – civil unrest stalled production till 2023 and in 2024 production was disrupted once again as the Kachin Independence Army seized control of key rare earth mining hubs, Panwa and Chipwe, leading to supply interruptions. Read more here.

🇦🇺 Australia – 13K M metric tons (Lynas leading the charge)

🇹🇭 Thailand: 7,100 metric tons - after Myanmar, the country is a major source of rare earth imports for China’s EV makers. They’re even building EV factories in the country, attracted by low tariffs.

The West’s Rare Earth Dilemma

The U.S. is heavily reliant on China, importing 80% of its rare earths (it must ship most of the ore mined in the U.S. to China for processing too)—a far bigger dependency than it ever had on Middle Eastern oil. Over the years the government has been working to change that, funding development of domestic separation plants - under a program started by Trump in his first term. But as with all infrastructure - building out those processing capabilities hasn’t progressed quickly.

In the meantime, China blocked the exports of 4 rare earths citing national security in 2023. And just days after the Trump 2.0 tariffs on China were introduced last month, Beijing hit back by imposing export controls on more than 20 critical minerals including graphite and tungsten.

A few days after the export controls kicked in, China’s Ministry of Industry and Information Technology released draft regulations which touched on issues — including quotas for mining, smelting and separating as well as monitoring and enforcement. The rules are the latest in a series of attempts to bring the globally critical sector under tighter Chinese state control.

China already dictates output via a system of quotas and state-controlled companies. According to the people much smarter than I, who understand the industry - The regulations are likely the consolidation of China’s production and processing industry which it has struggled to rein in for a while.

How to lose friends and alienate people

🇨🇦 Canada—Trump’s been picking fights with his dream 51(st) state. But it may behove him to remember it is home to one of the first in the wave of new western producers, looking to counterbalance the Chinese stranglehold on rare earths.

The government-backed Saskatchewan Research Council (SRC) started producing neodymium-praseodymium (never ask me to pronounce that) during the summer of 2024. The U.S.’s northern neighbour could quietly be holding the ‘Trump card’ in its stand-off with Washington afterall.

Newly sworn in Prime Minister Mark Carney is going to have to evaluate how to play that card, considering Canada has an estimated 14M metric tons of rare earths and could soon be a top 3 player in the rare earths world (dropping India down by a notch).

Case in point:

As Trump’s transition team was shaping up our wild ride of 2025 — in December of 2024, Canadian company Ucore Rare Metals scored $4M from the U.S. Department of Defence for a rare earth separation project in Ontario. The company is also building a facility in Louisiana to process ore from the U.S. and elsewhere —but conveniently inside a foreign trade zone, hedging against potential Trump-era tariffs.

Whether the Canadians will allow any of it, of course is a whole different question.

🇮🇳 India – and all the potential it has as a partner is now at risk, thanks to the sudden acrimony developing between the U.S. and India. India, as pointed out above currently has the third largest reserves of rare earths in the world. And they are largely untapped. Despite holding nearly 35% of the world’s beach sand deposits—a rich source of rare earths—India produced only 2,900 metric tons in 2023, less than 1% of global supply.

Mining and exploration are underway, led by Indian Rare Earths Limited (IREL), but the country’s full potential remains largely dormant for now. Investing in processing infrastructure and skills in India would mean a guaranteed source in a few years.

The industry experts will tell you - Rare earths aren’t rare, but processing is. And China still runs the game. But Australia, Canada, and the U.S. are gearing up for a shift.

As Amanda put it:

“We don’t get caught up in the hype. We just focus on what we do best.”

And focus is exactly what the West needs to do and fast, before the ‘distraction games’ leaves them eating Chinese dust.

Dropping the Processing ball

The elephant in the room: Processing.

You can have all the reserves in the world, but if you don’t have the infrastructure to process it, you might as well leave rare earths in the ground.

To build mining and processing infrastructure takes not just billions of dollars, but years of effort and of course permit processes that are relatively smooth. (let’s be honest, not that many countries can make bureaucracy easy).

Only a handful of companies make the cut for the kind of volumes we need in the rare earth sector. They include:

- 🇨🇳 China Northern Rare Earth High-Tech Co. Ltd: The largest, rare-earth company globally, with a market cap of $86.653 billion.

- 🇺🇸 MP Materials: Operates the Mountain Pass Mine, the largest, rare earth mine in the United States. The US currently only has one operating rare earth mine and processing facility in the country (& did I mention before that there is a Chinese stake in that company?)

- 🇦🇺 And of course, where this story began — Lynas Rare Earths: The largest non-Chinese rare earth supplier in the world.

The Century’s Biggest Deal—What’s Ukraine Really Packing?

All this brings us back to Trump-Zelensky rare earth dance for a “a big deal.”

Trump: “I told them [Ukraine] that I want the equivalent like $500B worth of rare earth. And they've essentially agreed to do that so at least we don’t feel stupid.”

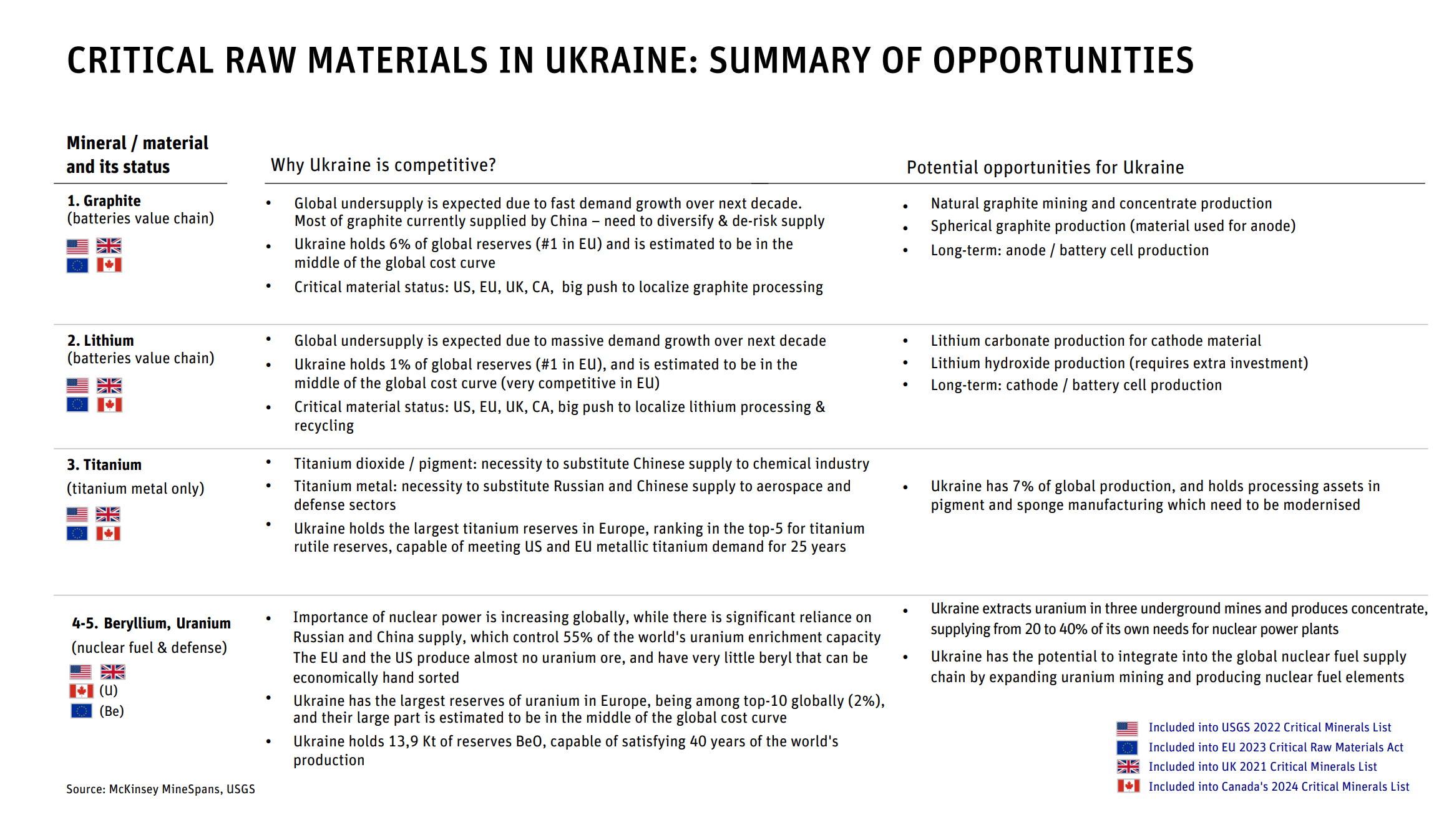

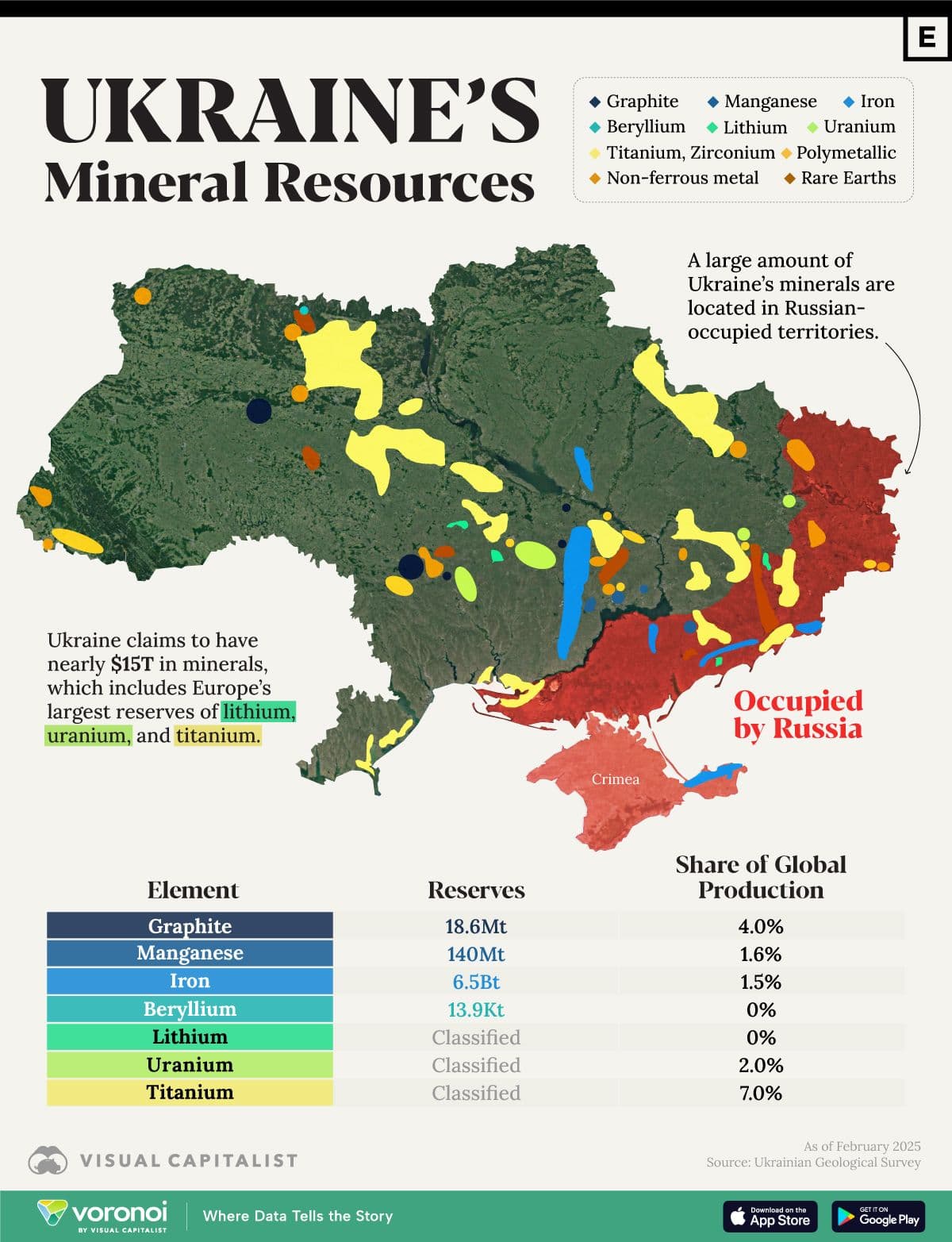

To hold a country hostage for its resources, those resources better be massive. But what is Ukraine really sitting on?

In 2022 Ukraine’s Environmental Protection and Natural Resources Minister Svetlana Grinchuk (then a deputy minister) claimed at a meeting of the UN Economic Commission for Europe (UNECE) the country possesses about 5% of the world's reserves of rare earth elements, despite occupying only 0.4% of the Earth's surface. And the Ukrainian government drew up decks to pitch its strategic competitiveness to investors.

The data from the Ukrainian Geological Survey is what the U.S. and EU have based much of their discussions on. But industry experts aren’t convinced about the valuation or reserve assessment.

According to S&P Global’s Market Intelligence: Ukraine’s rare earths data is based on outdated Soviet-era assessments. In fact, Roman Opimakh, former head of Ukraine’s Geological Survey, admitted there’s been no modern assessment of the reserves—and the information is still restricted due to security concerns.

Here’s the deal according to S&P Global:

Out of six rare earth deposits in Ukraine, only the Novopoltavske field in the Zaporizhzhia region has proven reserves with the license open for nomination. The large phosphate and rare earth deposit requires a $300 million investment, according to "Ukraine: Mining Investment Opportunities," a report by the Ukrainian Geological Survey and the Ministry of Environmental Protection and Natural Resources of Ukraine.

• The development of Novopoltavske, was abandoned post-USSR, and no progress has been made since after 13 years of exploration.• Other deposits in Donetsk, like Azovske and Mazurivske, are now controlled by Russia.• And some key data, like on scandium, is classified due to the ongoing war.

So, while Ukraine’s total mineral resources may be significant - its rare earths reserves are a toss up! They could be significant, or simply a cold war-era pipe dream.

The real value lies in how quickly the country can assess and verify the old surveys and data, currently being used as a bargaining chip for its security. Verification that is simply not plausible while the country is still fighting a war to survive.

The Russia angle

Vladimir Putin made a bold claim a few days ago on Chinese News network CGTN: Russia has more rare earths than Ukraine, and he wants the US to make a deal with them instead.

He’s not wrong on Russian reserves, but here’s the kicker: Russia’s rare earths production has flatlined for 5 years.

This week, after being shuttered for many years Russian authorities expect "specific decisions" on developing the Tomtor deposit (where’s that? Glad you asked - Click Here) of niobium and rare earth metals.

Tomtor is the key project in Russia's plans to boost output of rare earth metals, used in the defence industry and production of mobile phones and electric cars, to reduce its reliance on imports from China.

Before the Ukraine war. Russia had planned to invest $1.5 billion in rare earths, striving to become the biggest producer after China by 2030. The growth plan was driven through TriArk Mining, a joint venture with Rostec and billionaire Alexander Nesis (the oligarch heading the ICT group - Known to be close to the Kremlin, Alexander got his start in the late 1980s using uranium production waste from a mine in Uzbekistan to produce and sell rare-earth metals.)

But since 2022, it seems the Tomtor project has sat under the control of ICT group managers Vladislav Resin and Alexei Aleshin, with not a sign of Alexander. Perhaps the change of control of Tomtor is an indication of just how upset Putin was about the inoperational mine.

He seems to now be combining a vocal push to re-start production with offering tax breaks and loans to get investors and miners on board. The aim? Increase Russia’s share of global production from 1.3% to 10% by 2030.

The EU Snapshot

If you thought the U.S. hadn’t planned ahead, Europe is in an even worse position. To diversify away from China it has been on the hunt for rare earths for a while now, with not much to show for it.

After much hum and haw in 2023, Sweden uncovered reserves in an area called Kiruna. And in 2024, Norway reported an 8.8 million metric ton deposit—which is still under exploration.

But, wait for it… As Alf Reistad, CEO of Rare Earths Norway has pointed out - there’s no extraction in Europe right now. (Let alone processing).

EU + Ukraine: The Rare Earths Deal Before It Was Trending

The European Union has long been eyeing Ukraine’s rare earths, with a 2021 agreement that in March 2025 is now being revived. Ukraine holds deposits of 21 out of the 30 critical raw materials defined by the EU. Triggering the 2024 Critical Raw Materials Act, Brussels claims the deal it is offering Kyiv is more favourable than the White House offer.

But let’s rewind—back in 2021, the EU was already negotiating with Ukraine for access to its mineral riches, even before Russia’s full-scale invasion.

Europe has a 3–4-year head start over the U.S. in securing these resources, crucial for its most vaunted green energy transition and its newfound need to ramp up its own defence. The U.S. might be currently focused on political leverage, but Europe seems to be making the right noises needed to lock down Ukraine’s minerals.

History and shared values help cement long term deals and for Ukraine and Europe it goes even further back than 2021. Milestones like the 2014 EU-Ukraine Association Agreement, the 2016 Strategic Energy Partnership, and the 2019 Raw Materials Working Group might stand the EU in good stead — as long as it shows up with the security guarantees Ukraine needs.

Europe’s approach to Ukraine till now has been about long-term security and it can capitalize on its first-mover advantage. That is, as long as the Brussels bubble doesn’t want its own various drawn out ‘consultations’ and red-tape.

The Hold

The infrastructure challenge. Don’t expect quick results. New mines and processing plants in Ukraine won’t materialize overnight—greenfield projects take years. Which is why the EU needs to focus on deepening ties with Ukraine and creating a sustainable supply chain.

Any EU deal would need to be about more than just raw materials; it would need to be wider, especially keeping in mind the potential of the “raw earths” (I couldn’t help myself there!) data fizzling out.

A focus on securing future security for Europe, especially as the continent ramps up defence, maybe a wiser path to choose.

Final Thought

Since the draft deal between Ukraine and the US seems to indicate any agreement should not hinder Ukraine's European integration, the question is whether the U.S. will see Europe’s Critical Raw Materials Act as part of that process, or will President Trump label it as another “horrible” European move, with retribution required. And will Ukraine end up paying the ultimate price?

Only time will tell.

Going back to Amanda’s point - over the years there has been much ado about rare earth deposits on the moon, the seabed, war torn regions like Afghanistan and now Ukraine. In a geopolitically uncertain world, perhaps the time has come to focus on building the infrastructure to process the massive deposits already identified across the planet (including the U.S.) instead of indulging in “thought bubbles” at the cost of holding millions of lives to ransom.

Meanwhile, Amanda has got the rare earths covered if you need them. Just show her the money!

Experts in geopolitics, economics, technology, and society delivering sharp, concise analysis on the forces shaping our world.

More from The Chief Brief

View All → Conflict Watch

Conflict WatchMay 7th Broke Two Governments. Only One PM Got the Memo

Latvia’s PM Evika Siliņa resigns, In Britain, Keir Starmer is still in Downing Street. Just about.

Climate & Environment

Climate & EnvironmentFossil Fuel Exit Club

57 countries met in Colombia to agree on how to phase out oil, gas, and coal. The US, China, Russia, India, and Saudi Arabia were not among them.

The Macro

The MacroIMF Spring Meetings 2026: The $20 Trillion Report Nobody Talked About

The most expensive oversight of the week

Editor's Take

Editor's TakeEurope Is Being Rewritten. Here’s What That Actually Looks Like

From Budapest to Rome to Beijing: How Europe’s Political Certainties Collapsed in One Week

Get the Brief

Sharp analysis and global perspectives delivered to your inbox.

By subscribing, you agree to our Privacy Policy

Subscribe to The Chief Brief

Essential insights on geopolitics, business, AI, and society — delivered daily.

Subscribe to The Chief Brief

Essential insights on geopolitics, business, AI, and society — delivered daily.